The recent collapse of Silicon Valley Bank (SVB) in March 2023, the 16th largest bank in the United States, was a classic case of an asset – liability duration mismatch and a rapidly rising interest rate.

As the tech industry soared during 2019 to early 2022, SVB collected large deposits with no business deposit insurance, exploding the liabilities side of its balance sheet. Instead of investing deposits by offering lending to its customers which could have balanced their asset side partly, SVB invested in long maturity US Government bonds and Mortgage-backed securities, which are highly sensitive to rising interest rates. As interest rates rose during 2021-23, SVB’s bond portfolio lost substantial market value since its bond interest rate position was unhedged. Simultaneously, a large drop in the US Stock market in 2022, along with rising inflation, saw the tech industry stagnate after 2 years of robust growth, which led to large techs to withdraw their deposits. SVB was compelled to liquidate assets to meet its obligations, suffering big losses in its books. This liquidity crisis marked the beginning of SVB’s downfall. The Bank’s ALM strategy was regarded to be severely flawed.

Asset and liability management (ALM) is a long-term framework of managing financial risks (within risk appetite) that arise due to mismatches between the assets and liabilities as part of an investment strategy in financial accounting.

Assets and liabilities that are well-managed will lead to an increase in business profits. It reduces the risk of not meeting a company’s obligations in the future. It is relevant for the sound management of the finances of any organization that invests to meet its future cash flow needs and capital requirements.

According to the Society of Actuaries ALM Principles Task Force, ALM is defined as:

“Asset Liability Management is the ongoing process of formulating, implementing, monitoring, and revising strategies related to assets and liabilities to achieve financial objectives, for a given set of risk tolerances and constraints”.

Risks Mitigated through ALM:

ALM involves mitigation of a wide range of risks like Interest rate risk, liquidity risk, currency risk, capital market risk, regulatory risk etc. Two most common risks are as detailed below:

Interest Rate Risk

Interest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates.

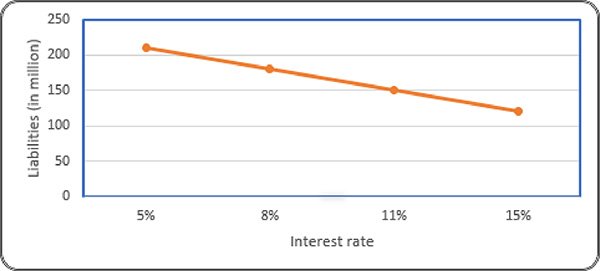

In Defined Benefit Plans, a decline in interest rate typically increases a plan’s liabilities (shown in the hypothetical example in figure 2 below)

Thus, ALM can help to reduce mismatching of assets and liabilities which occurs due to the fluctuation in interest rates.

Liquidity Risk

Liquidity is a measure of a company’s ability to pay off its short-term liabilities; those that will mature in less than a year.

As we know, short term employee benefits are offered to the employees such as compensated absences where payment is settled within 12 months of when employees render related services, for example, vacation, short-term disability, jury service, and military service. Liquidity risk can hamper such employee benefits plans.

To mitigate the liquidity risk, companies may implement ALM procedures to increase liquidity to fulfil cash-flow obligations resulting from their liabilities.

Currency risk covers risks associated with changes due to exchange rates. When assets and liabilities are held in different currencies, a change in exchange rates can result in a mismatch.

Applications of ALM in Pension Plans:

Pension obligations typically mature far into the future, hence their values are highly sensitive to changes in discount rates. In the Indian context, most employee benefit plans are of lump sum payout nature (Gratuity, Leave, LSA etc), also not all plans are funded (either by forming a Trust or with an insurer) due to no mandatory funding requirements yet. Thus there is inherent uncertainty in unfunded plans which may become a burden on the company’s cash-flow and liquidity. In either case, managing this volatility becomes even more important. ALM provides tools to manage funding gaps and contribution requirements where plans are funded Also pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets cannot be done appropriately.

ALM framework can help an employee benefit plan as follows:

- Quantifying investment risk and return

- Asset allocation – changes and optimal allocation

- Ensuring enough operating capital

- Long-term stability and profitability by maintaining liquidity requirements

- Managing credit quality